The Opportunistic Tranche

My Approach to Portfolio Construction

If you have not yet read our post #1 please go back and start there. We think you’ll find this post much more valuable within the context previously provided.

As discussed in our previous post, a significant portion of our portfolio is allocated to what we refer to as the Opportunistic tranche. In today’s post we will dive into this tranche to explain what it is and how we use it to maximize performance while limiting portfolio volatility and risk.

By the way, “tranche” is a term commonly used in finance; the word is French and generally translates as “slice” or “portion”.

To begin, let’s state the obvious questions that are likely on your mind:

why is that slice so large?

it sounds risky - what is the purpose of it?

is this an idea that’s been tested over time, or did you guys just make this up?

All great questions.

Our model portfolio and its opportunistic tranche is merely a modern-day version of the “60/40 portfolio” that has been used by wall street firms for more than 40 years. The standard 60/40 portfolio consists of 60% stocks and 40% bonds. The general idea of the 60/40 is this: since both bonds and stocks do well over time, and since these assets are negatively-correlated with one another, the combination of the two should provide excellent returns over time with reduced volatility, as compared to a portfolio of stocks only.

So far so good. However…

While that concept worked well from 1982-2021 — a very long time — with inflation now running hot for the first time since the early 1980’s what has occurred this year is that both stocks and bonds have gotten smashed at the same time and most investors have taken major losses thus far in 2022. In other words, the bond portion of the portfolio that was supposed to reduce volatility has actually added volatility to most portfolios over the past year — this new economic trend marked by persistent inflation and stock/bond correlation is likely to continue for the foreseeable future and represents a significant issue for most of the investing population.

Fortunately for those who understand this dynamic, there is an alternative. Our opportunistic tranche serves to solve this issue and has been an extremely valuable part of our portfolio — not just for the past year, but for many years.

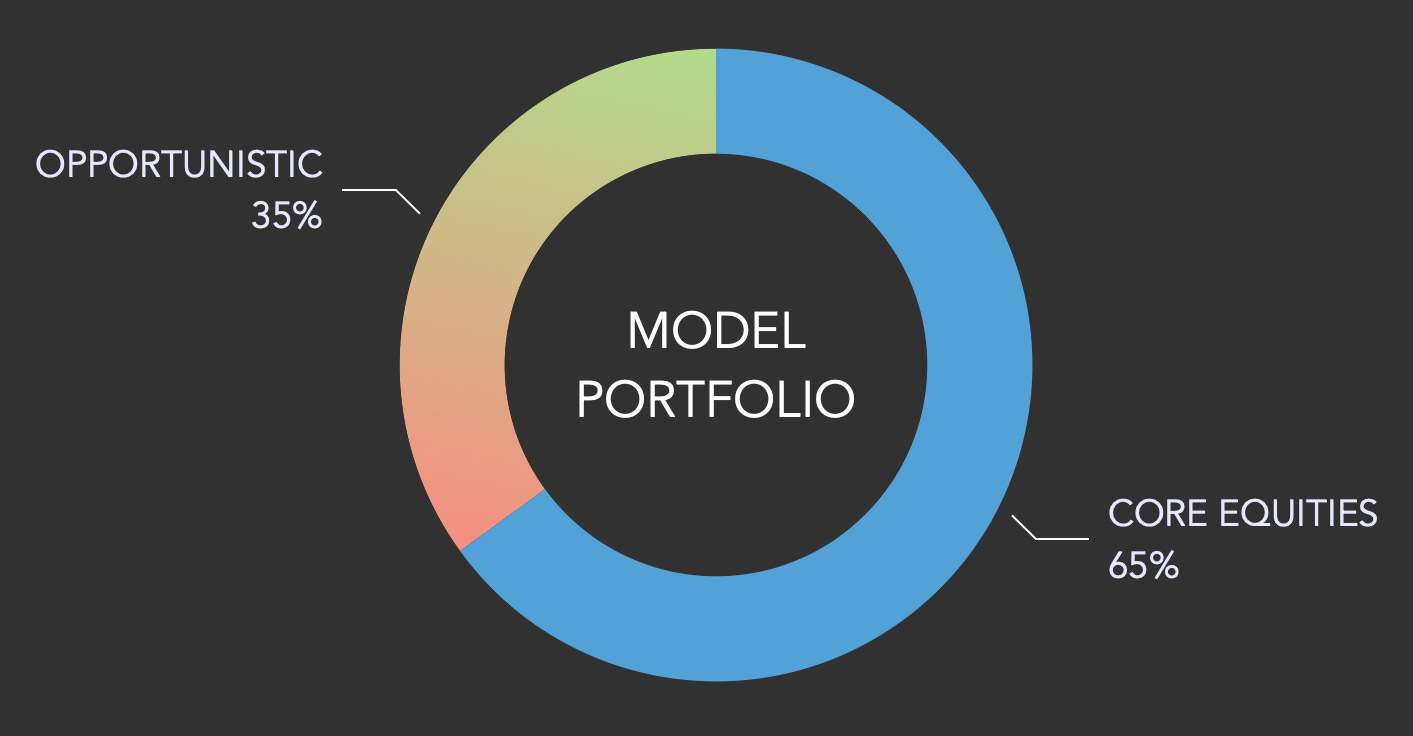

As depicted in the illustration above our portfolio is actually 65/35 and our opportunistic tranche replaces the “40% bonds” portion of the old 60/40 portfolio with assets we believe will properly complement our core equities given the current macroeconomic environment, whatever it may be. There will be times when this tranche actually does include bonds as discussed below, but there is a large selection of asset classes to choose from and our aim is to carefully select the assets we feel will best complement our core stock positions. It’s just a matter of understanding where we are in the bigger economic cycle, and we’re talking about the sort of cycles that last for years, not weeks or months.

We believe we are only at the beginning of a new trend where the 40-year long bull market in bonds has ended for this cycle as we believe there are a number of stresses in the fixed income markets that are systemic and likely not going away any time soon. A few of the factors at work here include a persistent inflation, a broken supply chain in a multitude of areas, a strengthening US dollar that is “breaking” the global financial system, and a US Federal Reserve (the Fed) that seems intent on creating much lower stock prices in the medium-to-longer term in order to slow the job market in the hope of suppressing inflation.

Unfortunately for most, the investment industry at large is fully wrapped around the idea of the old 60/40 portfolio and that will not change any time soon.

To summarize our answers to the 3 questions above: our opportunistic tranche is sized in a manner that has been tested for decades, it is not something we just made up, rather it is a modern-day approach to an outdated strategy, and this tranche exists purely to reduce portfolio risk and volatility while allowing for upside gains.

CURRENT ALLOCATION WITHIN OPPORTUNISTIC TRANCHE

As mentioned in our previous post #1, our opportunistic tranche currently consists of a small basket of emerging market stocks and other securities that we believe will significantly outperform in a weak-dollar environment. Given that the US dollar continues to be in a strong bull market, these positions are currently quite small while we continue to add to our positions over time.

As we look out over the coming months and years we see US stock indexes that will likely remain relatively weak, a US dollar bull-market that will eventually end, a Fed that will almost certainly fail to quash inflation and begin “printing money” again, a world that will be in desperate need of mining for more materials for green energy in whatever form it may take, a China that will someday end its disastrous zero-Covid policy and a need for fossil fuels that will not soon end.

With all this in mind let’s take a look at the 5 major components of our opportunistic tranche:

Cash: As shown in Illustration 2 below, currently cash is by far our largest position in this tranche - and cash has served us well throughout this year. While cash is boring, it is easily the best place to be when equities, fixed-income, and commodities are all weak. We continue to put cash to work on nearly a daily basis as our favorite asset for the long term continue to get cheaper and cheaper.

Emerging Markets: We have been slowly building positions in emerging market equities over the past several months and will continue to do so. The strong US dollar and China’s seemingly endless zero-Covid policy are among the circumstances that continue to contribute to the decline in these assets and we believe continued accumulation into this weakness will pay off well in the coming years. Currently our primary focus is on shares of companies based in China, Taiwan, India, and many of the smaller economies that circle the Indian Ocean, from Africa to Southeast Asia.

Commodities: While we sold all our commodity positions earlier this year with the exception of a very small position in silver, we expect the coming months to provide opportunities to begin building positions in this sector with primary focus on copper, oil, rare earth metals, gold, and silver. Commodity prices can be extremely volatile and our holdings for this asset class will be sized accordingly.

US Treasuries: Notwithstanding our longer-term bearish outlook for this asset class, we have been building a position in long-dated treasuries since early September as we expect interest rates to be driven significantly lower during what appears to be a coming sharp downturn in economic activity. This would represent a cyclical bull market in Treasuries during what we believe will be a continued secular bear market in bonds.

Long & Short US Stock Indexes: We will look to be long US index ETFs at times when we feel US stocks are in a cyclical bull market, while looking to take short positions on US equities to take advantage of significant market downturns. This particular portion of our opportunistic tranche has been quite active this year and has contributed nicely to our strong relative outperformance this year

Illustration 2. Current portfolio holdings, high-level view. 10/22/22

OUR PERFORMANCE YTD

As of October 22, 2022 our portfolio is -3.44% YTD compared with the S&P 500 -21.20%, the Nasdaq composite -31.43% and the Russell 2000 -23.33% for the same period.

We are particularly proud of this result as our portfolio was much heavier-weighted in equities during the first half of this year as we took in solid dividends while shorting the US equity markets against our long positions.

We feel we are in a good position to close the year in strong fashion both relative to the S&P 500 as well as in absolute terms pending the market action for the remainder of 2022.

PLEASE NOTE WE ARE NOT SUGGESTING YOU TRY TO MIMIC OUR PORTFOLIO AND WE ALSO DO NOT EXPECT OUR READERS’ PORTFOLIO PERFORMANCE TO MATCH OURS IN ANY WAY.

WE PROVIDE OUR PORTFOLIO ONLY TO ADD CONTEXT TO THIS POST. PLEASE DO NOT BUY OR SELL ANY INVESTMENT PRODUCTS BASED ON THIS PUBLICATION!

IN CLOSING

If you have any questions or if you want to continue the discussion about this post please Comment or join our free Chat, and visit our “About” section to learn more about FiNiche.

DISCLAIMER

FiNiche and it’s team members are not licensed investment advisors. Nothing produced or discussed under the FiNiche brand should be construed as personal investment advice. We do not benefit from, nor do we make solicitations related to, the buying or selling of securities or any other investment products. Information provided by FiNiche is intended for general informational, educational and entertainment purposes only. Please do your own research and be sure you have a solid plan before putting a dime of your money into these crazy markets.