The Big Portfolio Refresh, March 2023

The Original Cocaine Bear, and Markets High on Passive Investing

It’s really important for people to understand ‘how’ to trade and ‘why’ to trade before thinking about ‘what’ to trade. The ‘what’ is an easy, and in many cases lazy solution. — Grant Williams, Feb 2023

In this issue:

FOREWORD

SIGNIFICANT OBSERVATIONS

Retail Investors Gone Mad

Global Liquidity Downturn

Inflation Update

Fed Speak

High-Yield Cash Equivalents

China Sanctions US

MARKET OUTLOOK

Overview

Holdings Spotlight

Additional Charts

MY PORTFOLIO

Portfolio Objective

Asset Allocation

Current Holdings and Rationale

Composition Highlights

Recent Trades

Performance

ETF-only Portfolio Alternative

FOREWORD

It was 15 years ago this month. I was in my late 30’s sitting on a trading desk at Merrill Lynch watching Bear Stearns implode. It was one of the earlier dominos to fall in what was to become the Great Financial Crisis (GFC).

It was the first time I fully realized just how impactful major market events can be on the actual lives of real people.

To be clear, I don’t think we are on the precipice of another 2008-style market crash. Nonetheless that’s where I begin this short story in an attempt to explain why I do what I do.

In the aftermath of the GFC, working people in their 50’s and 60’s saw their retirement savings wiped out and had to rethink their later working years. College savings for their kids were wiped out as well. I watched as many people lost their homes, their dignity and their livelihood. And as poverty quickly became rampant in many neighborhoods across the US and around the world, some even lost their life.

Honestly the whole thing was far, far worse than the recent Covid experience of 2020, but it’s not like the crash that began in October 2008 came out of nowhere. The signs were everywhere. And the signs were spread out over the course of many months, in fact well over a year, and were on full display for anyone paying attention.

It was actually back in February-March of 2007 that the subprime mortgage industry collapsed with several lenders declaring bankruptcy, announcing significant losses, or putting themselves up for sale.

Unbelievably, 6 months after that, the S&P 500 hit an all-time high on October 15, 2007 — the euphoria of the investment public was insane.

Five months after that new market high in late ‘07 and heading into the weekend of March 14, 2008 Bear Stearns sat on the edge of bankruptcy. On that Sunday JP Morgan, assisted by the US government, bought the 85-year-old investment bank for just $2 per share. It was a shocking moment for any Wall Street historian.

But at that point, the S&P 500 was only down ~14% from where it began the year and by mid-May the index had rallied all the way back to ‘even’ for the year.

To broadly summarize the rather long timeline:

The subprime mortgage market collapsed in early 2007

The S&P 500 reached an all-time high in October ‘07

Bear Stearns collapsed in March ‘08

The S&P 500 rallied back to its ‘08 high by mid-May

Fannie Mae and Freddie Mac had to be taken over by the US government in early September

Then, in a single week spanning Sep 15 - Sep 22: Lehman Bros collapsed, the Fed took over AIG, the Fed’s primary fund “broke the buck” nearly crashing all money market funds, Bank of America bought the near-bankrupt Merrill Lynch, investors withdrew $144 billion from US money market funds, the Fed begged Congress for $700 billion to bail out the banks, Goldman and Morgan Stanley converted from investment banks to commercial banks to increase their protection by the Fed, and Morgan was acquired by the Japanese MUFG bank

Unbelievably though, the big market crash that ended up defining a generation did not begin until October.

So even if you missed or did not understand the subprime market, you still had 18 months to prepare, and still 7 months following the Bear Sterns collapse and lots of other bad news along the way.

And as if that was not enough, you still had another 10 days following that Sep 15-22 period to sell your risk assets before the big crash began.

So there was more than enough time for people to pay attention, to ask questions, to study, to seek guidance and make changes — and yet almost everyone missed it. In October ‘08 alone, the S&P lost ~30% of its value, another 12% in November, and by March 2009 the whole thing was over with most assets and most people just plain wiped out. The markets did not completely recover until 2013.

Even the most senior advisors in my office at Merrill lost most everything they had worked their whole lives for and ended up facing significant life changes and very difficult personal decisions as a result.

Fortunately, with my own money and my clients’ money, I had the foresight to avoid the entire market crash. I sold all my stock and all my clients’ stock by June of 2008. Admittedly, the 4 months I had to wait to be “right” was really tough — at the time it seemed like an eternity.

I tell this story to make a simple point: those who pay close attention to what’s in front of them will never be caught completely off-guard.

Of course market crashes like that are quite rare. In fact, I do not see anything of that sort on the horizon nor is that something I am specifically preparing for.

However, the reason I do not see that sort of event playing out again, is precisely the reason for my concerns regarding market volatility, and the potential for ever-increasing episodes of the sort of waterfall sell-off in stocks we saw during March 2020.

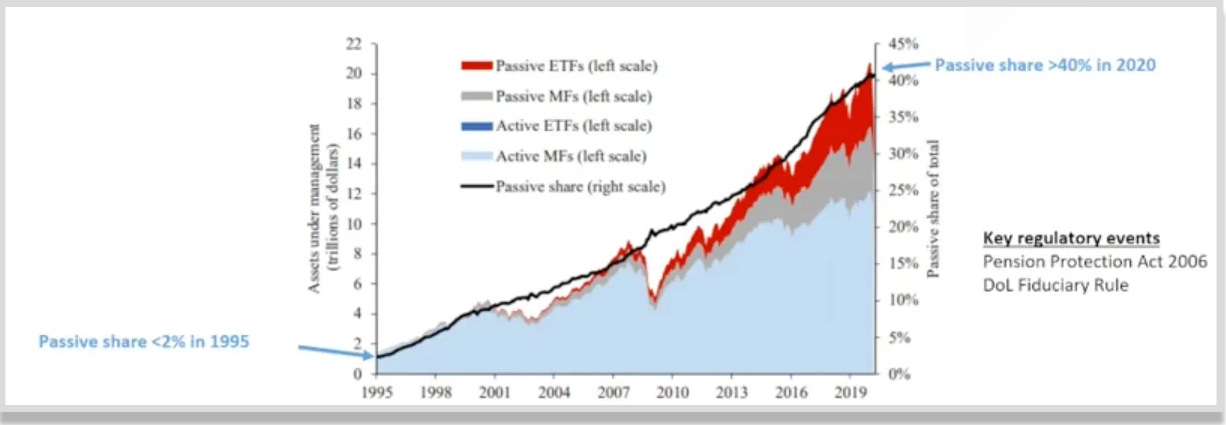

And I can sum up the new demon bubbling beneath the markets in two words: Passive Investing.

The growth of passive strategies, particularly over the past decade, has changed the underlying market structure so significantly that it’s critical for a money manager to be both aware of the issue and knowledgeable about potential solutions for protecting a portfolio of investments.

The idealogical ‘benefits’ of passive investing were initially derived from the Efficient Market Hypothesis that states if markets represent the sun total of information that is available, then any attempt to try to outperform is going to be futile because the aggregate of all information is already priced into stocks.

Passive investing allowed the Vanguards and Blackrocks of the world to take on massive inflows without having to manage portfolios. For the funds of those companies, the ‘strategy’ was simple: if you give them money, they will buy; if you ask for money, they will sell. Valuations, fundamentals and technicals do not matter in that world. For my younger readers, keep in mind that mutual funds — which had been very popular as early as 1980 — were never intended to work that way. Fund managers were not forced to buy anything just because you gave them money to invest.

Today, it is estimated that nearly half of all trading in the US equity markets is some form of passive investing. The implications of this are astounding and are right in front of your eyes if you care to look.

John Bogle himself (founder of Vanguard) said of passive investing in May 2017:

“If everybody indexed, the only word you could use is catastrophe - the markets would fail”.

These are some of the more significant impacts of passive investing on markets:

Increase in correlation between securities, particularly in securities that are part of the same index, sector or other logical grouping

Increase in valuations of securities, regardless of fundamentals, as passive shares grow

Reduced market elasticity raises risks of extraordinary price movements (e.g., March 2020 flash crash)

Increases in market concentration as momentum bias leads to largest companies becoming larger (e.g., this is how Apple became a $3 trillion company)

Reduced ability to new companies to be come public

As a result of passive investing, the largest 7 companies by market cap comprise ~50% of the NASDAQ Composite index. Just 6 of those 7 comprise nearly 25% of the S&P 500. So when you hear people saying “the market is up” or “the market is down”, understand that what they are looking at is an index, and that index is primarily a small handful of companies.

It is important to understand why passive investing has grown into the monster it has become. It’s not just because people want an inexpensive way to gain market exposure.

There have actually been huge regulatory changes that have driven the growth of passive investing because it has been perceived to be this innocuous benefit to most consumers of investment products.

The Pension Protection Act of 2006 introduced the qualified default investment alternative in 401k’s which basically put a company’s HR department in charge of choosing your investment elections; over time those investment elections have become more and more uniform with fewer choices.

Target funds and index funds are about all that is left in most 401(k)’s. Another regulatory change in 2012 made target date funds universal in within 401(k)’s. In fact, ~85% of every 401(k) dollar now goes into target date funds.

What we are left with then is basically the majority of investors all acting as a single entity, buying and selling the same products whose underlying securities are primarily the largest companies.

Now if you know all of this, and you understand how the markets work, you can use this to your advantage.

The investment strategy that I’ve developed over decades has been shaped by the rise of passive investing. Knowing that the US stock indexes are driven primarily by just a few stocks, I use a long-short-index strategy to complement my core equity positions for both risk management and alpha generation as appropriate given market conditions.

That is one of the strategies I employ in my within the ‘opportunistic tranche’ of my portfolio. My core equities tranche has little exposure to the mega cap stocks that drive the indices and focuses primarily on stocks that I perceive to be trading at appropriate valuations with good technicals and solid fundamentals.

More on my portfolio construction further down the page here.

All of this serves not only to reduce volatility, but to also provide a more stable stream of income and growth over the longer term.

You can see the results of this approach in my performance numbers I share later in this post. My portfolio remained very stable and nearly flat for all of 2022 while the indexes and most stocks and bonds got clobbered.

While I don’t consider myself to be an expert on anything — and I have certainly been wrong often enough to stay humble — after 30 years of managing money I have developed my own unique approach to portfolio management that I feel very comfortable with, and I want to continue to share my knowledge with anyone who has the time and desire to learn.

Let’s dig in.

SIGNIFICANT OBSERVATIONS

RETAIL INVESTORS GONE MAD

As shown in the chart below, retail investors poured more than $1 billion per day into US markets during January.

This period included some of the highest daily amounts ever recorded as shown in the next chart here.

Such bullish sentiment by retail traders is reminiscent of the entirety of 2021 as US stock indexes soared to new highs during the covid-era melt-up. I suspect the continued drawdown in global liquidity will bring the retail crowd to its knees before this year is over.

GLOBAL LIQUIDITY DOWNTURN

Global liquidity conditions remain the tightest they have been for several decades, continuing to pose a formidable headwind for most equities.

Liquidity is probably the most important short- and medium-term driver of risk assets. In fact, the fundamental value of an asset can become moot, if only for a short time, at periods when market liquidity dries up.

Nonetheless, as mentioned above the retail crowd continues to YOLO and FOMO into la-la land. I’m guess that will not end well for most.

INFLATION UPDATE

Whether we are in a long-term persistent inflationary environment or not is unknowable and honestly it does not matter to me in terms of my portfolio. However what IS important is the current narrative about inflation, the likely short-term future trend, and the Fed’s response to the data coming out — because that is what continues to drive stocks up and down with volatility.

After a hotter than expected consumer price inflation (CPI) print for January, the producer price index (PPI) also came in hotter than expected, up 0.7% MoM, which pushed the YoY rise to +6.0%. The index for final demand goods moved up 1.2% in January, the largest increase since rising 2.1% in June 2022.

In the charts below we can see that price inflation on both the consumer and producer sides has remained persistent since the covid lockdowns of 2020.

It is important to note, however, that nearly one-third of the January rise in the index for final demand goods can be traced to prices for gasoline, which increased 6.2%. The indexes for residential natural gas, diesel fuel, jet fuel, soft drinks, and motor vehicles also moved higher. Conversely, prices for fresh and dry vegetables decreased 33.5%. The indexes for residual fuels and for basic organic chemicals also declined.

On Feb 24 we got the PCE (personal consumption expenditures) report which also came in hotter than expected, leading to a fairly dramatic selloff in US stocks as the implication is this allows the Fed to remain on the hawkish side of its narrative for now.

FED SPEAK

After a hot PPI report on Feb 16, Cleveland Fed President Loretta Mester rubbed salt in the wounds of the market this morning when said she saw a compelling case for rolling out another 50 basis point hike earlier this month and the US central bank has to be prepared to move interest rates higher if inflation remains stubbornly high.

“At this juncture, the incoming data have not changed my view that we will need to bring the fed funds rate above 5% and hold it there for some time,” Mester said Thursday in remarks prepared for an event organized by the Global Interdependence Center and the University of South Florida Sarasota-Manatee.

“Indeed, at our meeting two weeks ago, setting aside what financial market participants expected us to do, I saw a compelling economic case for a 50 basis-point increase, which would have brought the top of the target range to 5%.”

Additionally, as Bloomberg reports, Mester said inflation risks remain tilted to the upside because of the war between Russia and Ukraine, which adds more uncertainty for food and energy prices. China’s reopening could also increase demand for commodities, she said.

To summarize then, the S&P 500 sold-off quite sharply following the Feb 1 FOMC meeting, the Feb 16 comments above, and the Feb 24 PCE report.

HIGH-YIELD CASH EQUIVALENTS

If ever there was a free-lunch in the financial markets, here is something we have not seen since ~1999. That is to say: with stock valuations still high on a relative historical basis and a global economy that continues to slow, you can actually get a good return on short duration cash equivalents. As shown in the chart below, the 1-year US Treasury bill is currently paying 5.05%.

If you are not familiar with buying treasuries, no problem. The easiest way to take advantage of this set of circumstances is to check with your broker about available money market funds. Some online brokers offer money market funds paying more than 3% APY. This may be a good option for those who want a place for their cash while waiting to move that cash back into risk assets when the time is right. Getting in and out of T-bills is a bit more complicated of course.

CHINA SANCTIONS US

As reported by Reuters on Feb 16:

China on Thursday put Lockheed Martin and a unit of Raytheon Technologies on an "unreliable entities list" over arms sales to Taiwan, banning them from imports and exports related to China in its latest sanctions against the U.S. companies.

The measures come amid heightened tensions after the U.S. military shot down what it says was a Chinese spy balloon, and a day after Beijing warned of "countermeasures against relevant U.S. entities that undermine China's sovereignty and security".

Lockheed Martin Corp (LMT) and Raytheon Missile and Defense Corp, a subsidiary of Raytheon Technologies Corp (RTX), are prohibited from "engaging in import and export activities related to China," China's commerce ministry said in a statement.

"These are symbolic measures and unnecessary - that's how we view them," White House press secretary Karine Jean-Pierre told reporters on Thursday.

While this is likely not impactful for LMT or RTN stocks, the sanctions are yet another new example of the tightening tensions between the US and China. At the core of those tensions, I would argue, is the increasing frustration by China, Russia, and their allies of the US’s use of the US dollar and SWIFT system as a weapon of economic war.

Keep in mind that the reason for the US dollar’s dominance in the world stems 100% from our success in the two world wars of the 20th century, the US military build-up since then, and the ~50-year-long need for countries around the world to bankroll US Treasuries to by oil from Saudi Arabia since 1973.

As one of my favorite investors pointed out back in 2019, the reason the US has been so successful at maintaining it’s dollar dominance is that we are the first nation with such power to use that power responsibly — weaponizing our currency only in exigent circumstances. But over the past decade the list of US sanctions is so long I am not going to take time here to even begin discussing that list.

The concern now for the US government is that the dollar, which has been very strong since 2015, may ultimately crumble under its own weight as other countries around the world (e.g., China, Russia, their allies) decide they’ve had enough. The Petro-yuan and the growing relationship between China and Russia is a great example of how this is all beginning to unwind.

This is only part of the story and I feel that somewhere within the Russia-Ukraine conflict (which I see as a China-US proxy war on some level), this will all eventually come to a head. And it ain’t gonna be pretty.

MARKET OUTLOOK & MY PORTFOLIO

I heard the below on one of my favorite podcasts last week when the discussion turned to potential market volatility should the Fed over-tighten monetary policy:

“And if that is the case sir… we're going to see assets switching at an insanely rapid rate where you're going to want to go from owning no bonds to all bonds, to no duration stocks to all duration stocks, in rapid succession. And wealth can get eviscerated in that environment, particularly if it isn't actively managed.” — Julian Brigden, Feb 23, 2023

Twice-a-month I revise and publish my comprehensive market outlook along with lots of details around my portfolio (see table of contents above).

If you are not yet a paid subscriber you are welcome to view a recent free post to get an idea of the sort of detail I provide for my paid audience. For details around subscription tiers, please click the button below or visit my About page.

Keep reading with a 7-day free trial

Subscribe to FiNiche Investments to keep reading this post and get 7 days of free access to the full post archives.