Inflection Point

Market Minutes: Macro Update & Portfolio Brief

Following my Big Portfolio Refresh of Nov 29, I’m bringing you the latest developments pertinent to my investment portfolio.

In this issue

Macro Update

Monetary Policy

The Labor Market

Historical Market Trends

Short-Term Technicals

Impact on Investors

My Portfolio

Recent Portfolio Moves

Asset Allocation

Performance

MACRO NOTES

MONETARY POLICY

Like it or not, markets continue to move strongly with FOMC narratives so once again we begin here.

On 11/30 Jerome Powell took to the stage to provide some guidance as to where monetary policy may be headed in the short-to-mid-term. If you like you can read the entire transcript; here are some excerpts from the Chairman’s speech:

“The report must begin by acknowledging the reality that inflation remains far too high — it will take substantially more evidence to give comfort that inflation is actually declining — the truth is that the path ahead for inflation remains highly uncertain — we need to raise interest rates to a level that is sufficiently restrictive to return inflation to 2 percent.”

“We are tightening the stance of policy in order to slow growth in aggregate demand. Slowing demand growth should allow supply to catch up with demand and restore the balance that will yield stable prices over time. Restoring that balance is likely to require a sustained period of below-trend growth.”

“For the near term, a moderation of labor demand growth will be required to restore balance to the labor market.”

“Growth in economic activity has slowed to well below its longer-run trend, and this needs to be sustained.”

The Fed likes to use intellectual slight-of-hand rather than just explain things simply, but everything Powell said here appears to be inline with our expectation of another leg lower for US stock indexes.

As you will see below, I continue to take profits into this bear market rally and I look to add to my short positions opportunistically.

I expect the Fed to announce a 50 bps rate increase next Wednesday, and likely follow with 25bps Feb 1, and 25bps again in March, perhaps pausing after that.

THE LABOR MARKET

As illustrated above, the labor market holds the key to the FOMC direction with monetary policy and therefore, with stock index levels.

On 12/2 we got the latest jobs report. Non-farm payrolls rose by 263,000 with unemployment holding at 3.7%. On the surface, the report suggests a healthy labor market but when you look below the surface you can see there are issues beginning to mount.

It’s important to note that real job creation is actually trending down with statistical anomalies making the report look better than it actually is. Here are some highlights:

Most jobs were created in leisure and entertainment, education, healthcare and the government. It makes perfect sense for leisure and entertainment to continue to play catch-up following the long period of lockdowns, so let’s disregard that for now. Jobs in government, education and healthcare are not typically indicators of a growing economy where you would typically see job growth in economically sensitive sectors such as manufacturing, retail, transportation and housing.

The jobs participation rate remains extremely and persistently low; remember that people no longer looking for a job are not counted as unemployed. Of course people without jobs tend to spend less money which creates a drag on the economy.

Non-farm payroll growth continues trending lower on a momentum basis as viewed by 3-month and 6-month moving averages

As indicated by Powell in his 11/30 speech, the Fed clearly wants the unemployment rate higher and they are tightening monetary policy to that end — and yes, it appears to be working. However, with unemployment a lagging indicator, the Fed is likely to push rates a bit higher and hold them there longer until the stock market, the housing market, and employment reach their desired levels.

HISTORICAL MARKET TRENDS

As we learned from David Rosenberg on the Macro Voices podcast #352, there are patterns that constantly reemerge in a recessionary bear market when we are close to the bottom of the cycle. Here are two:

In a recessionary bear market, the market finds its bottom as the recession itself becomes a well known, much talked about fact — this is the time when the market will start pricing in a recovery. Clearly a recession has either only just begun or has not yet even begun, so in the context of this example markets can be nowhere near a bottom if a recession is indeed on the way.

Bear market bottoms tend to occur when the Fed is ~70% into an easing cycle when interest rates have been sufficiently reduced to re-steepen the treasury yield curve; there has never been a period in history when a bear market bottomed while the Fed was still raising rates. Currently the yield curve is quite inverted along much of the duration range and the Fed is still raising rates. Again, in this context markets can be nowhere near a bottom.

Additionally, as discussed by Financial Sense this week, market pivots are generally associated with cyclical economic or monetary pivots — this is in concert with Rosenberg’s views above. In the chart below we can see that neither the ISM Manufacturing nor the monetary indicator seems to have found a bottom, also signaling that we have not yet seen the lows for the current bear market.

TECHNICALS

As I predicted in my previous post, the SPY indeed moved up into the ~410 area immediately following the 11/29 Powell speech, but has since fallen to confirm a short-term breakdown of the uptrend that began Oct 13 (red line “D” in the chart below).

With the CPI numbers coming out on Tuesday next week and the FOMC announcing their monetary decision on Wednesday, it is no surprise that the broader US market appears to be sitting at a significant inflection point. I expect to see some fireworks, in one direction or another, as the news rolls out.

Moving to the petroleum market, I took a look at the long term price history of WTI (West Texas) crude oil. The chart below goes back to 2002 and we can see that the long-term mean price is ~$60 per barrel. If we are indeed heading for a recession at some point in 2023, I can see where oil may soon find that $60 price again, and perhaps lower — regardless this is still one of my favorite investment sectors as described more fully in my “Of Earth and Isotopes” article.

Despite the down-trend in oil since topping at $130 in March upon the Russian-Ukraine conflict, the oil pipeline companies that I hold in my portfolio have performed quite well as expected. Using the MLPX ETF as a proxy, you can see the solid price pattern in these stocks since the March 2020 “covid bottom”. Of course these stocks are likely to pull back with the rest of the market as a recession draws nearer, at which point I will likely add to my positions.

I also want to show you the materials miners price action, using the COPX ETF as a proxy for the stocks in my portfolio. As discussed in my “Of Earth…” article, along with oil I have good exposure to the companies involved in extracting raw materials from the earth. Those stocks also continue to do well as seen the chart below. As with my energy stocks, these stocks are likely to pull back with the rest of the market as a recession draws nearer, at which point I will likely add to my positions.

IMPACT ON INVESTORS AND MY PORTFOLIO

I am revising my macro update slightly since the last time I wrote.

My base case continues to be that the US stock indexes will see lower lows before this bear market is over; likely in Q1 2023. However, on the back of what is likely to be a more dovish Fed narrative at those lower lows, I feel that stocks may begin an incredible cyclical bull market that could go into 2024.

To be clear, I do not see the S&P 500 or the NASDAQ Comp making new highs as a secular bear market is likely to remain intact. However, as I discussed in my previous post, a secular bear market is likely to be filled with extreme volatility in both directions, frustrating the 60/40 and buy-and-hold investors alike.

The time for active management arrived one year ago, and I continue to believe it is here to stay for some years to come.

As always I take things one day at a time while looking for the best opportunities to invest while keeping my eyes on the charts to take advantage of moves in both directions, to the extent possible.

And with that, let’s dig into my Portfolio!

The below portion of this newsletter is still being offered free of charge to all my readers. Please see my About page for subscription tiers coming in ~March 2023.

MY PORTFOLIO

FIRST, A CAUTIONARY NOTE

I know that some of my readers are experienced enough to translate the content of this newsletter into actionable steps for building and managing their own portfolio tailored to their own needs. However I also know that some of you may lack proper experience and the last thing I want to do is mislead anyone.

The information provided here is:

Intended to put my macro framework into context for the experienced investor

Not to be construed as investment advice for any specific individual

Recent portfolio moves

I have been quite active in my portfolio over the past couple weeks, in particular on 11/30 and 12/1 as I reduced risk by taking gain following the sharp move higher in stocks the followed Powell’s speech. Thus far that has proven to be a fortuitous move.

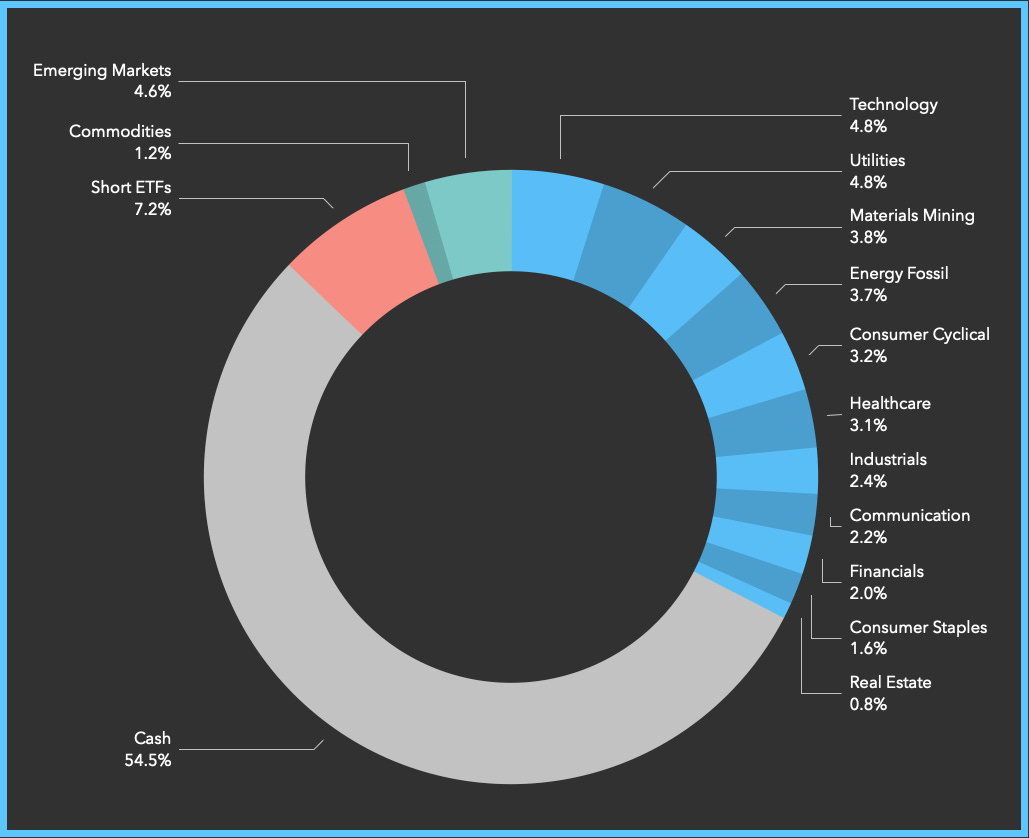

Comparing my current portfolio to that of my previous post on 11/29, I have reduced my long equities exposure from ~30% to ~24% as I brace for the next leg down that I am expecting.

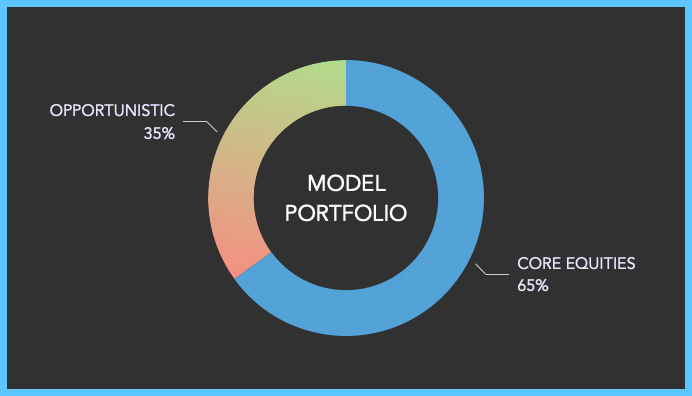

Model portfolio allocation

In previous posts I discussed at length both the overall construction of my portfolio as well as its ‘opportunistic tranche’ in more detail. I encourage you to go back and read those pieces to better understand my approach.

Actual portfolio allocation: high-level view

Performance

Current holdings

I detail my specific stock and ETF holdings in my monthly Portfolio Refresh, the next edition of which will be published on January 1. In the meantime, you can see my holdings in my previous Refresh if you like.

IN CLOSING

If you have any questions or if you want to continue the discussion about this post please comment or join my free Chat, and visit my About section to learn more about FiNiche including how to contact me directly.