Off to the Races

Off to the Races

Mid-Month Market Minutes: Significant observations & portfolio impact

In this issue

SIGNIFICANT OBSERVATIONS

The January Effect

The Last Domino

No Rate Cuts in 2023

Labor Market

Consumer Price Index

No Soft Landing

Historical Market Trends

Additional Charts

Impacts for Investors

PORTFOLIO IMPACT

Portfolio Objective

Updated Asset Allocation

Performance

FOREWORD

My portfolio is off to a good start in 2023. A combination of value stocks and US index short positions continues to provide stability in a sea of global market chaos.

After ending 2022 less than 1% lower — far ahead of global stock indexes and most hedge funds — I feel my portfolio and investment strategy are set on the right path for continued success in 2023.

I encourage you to go back and read my Dec 31 post for my full macro view on the markets - there is a lot in there and you’ll want to keep all of it in mind as we move along. tip: if you have an iPhone just use the two-finger-swipe-down and have Siri read to you - like a poor man’s podcast :-)

This article is part of my mid-month ‘Market Minutes’ series and is intended as a supplement to my Big Portfolio Refresh; providing timely updates around significant market-moving events. My next ‘Big Refresh’ will be released on Feb 1.

SIGNIFICANT OBSERVATIONS

THE JANUARY EFFECT

Both stocks and bonds are off to the races in 2023 with the January Effect in full swing as I had suggested in my Dec 31 post. The S&P 500 is +4.22% on the year as the 10 yr US Treasury yield has fallen from 3.88% to 3.50%.

The S&P 500 now sits at a critical inflection point as indicated in the charts below.

As promised, during the current rally I have been reducing my overweight stock positions back to equal weight while adding to my short positions to decrease my overall net-long exposure to risk assets. I continue to believe we’ve yet to see a real bottom in the broader US stock market.

THE LAST DOMINO

Apple (AAPL), the largest component of both the Dow 30 & SP 500 and the last holdout of the mega-cap tech stocks — finally began a meaningful descent on Dec 21. The stock confirmed a breakdown below long term support and now appears to be in the process of a much overdue repricing of the security.

Apple peaked at a frothy market cap of ~ $3 trillion and will likely see a 50% haircut before finally finding a bottom.

While I do not own AAPL, this move is significant within my portfolio as my short positions in US equities benefit from a sell-off of the largest names within the index — Apple being the biggest of them all.

And with much more downside likely for this stock and the US indexes, I will continue to trade my short-equity positions within my portfolio’s opportunistic tranche to offset overall volatility to the extent possible.

FED: NO RATE CUTS IN 2023

Jan 4: Minutes from the central bank's December policy meeting released Wednesday showed that while Fed officials welcomed easing October inflation data, they stressed it would take substantially more evidence of progress to be confident inflation was coming down in a sustained manner.

No Federal Reserve officials thought it’d be appropriate to begin cutting rates in 2023, and officials worried easing financial conditions could complicate the central bank's efforts to bring down inflation.

This is consistent with the summary of Jerome Powell’s statement of 11/30 which is included in my “Inflection Point” post and pasted below. This is also consistent with my view that major US stock indexes have yet to find a bottom.

“The report must begin by acknowledging the reality that inflation remains far too high — it will take substantially more evidence to give comfort that inflation is actually declining — the truth is that the path ahead for inflation remains highly uncertain — we need to raise interest rates to a level that is sufficiently restrictive to return inflation to 2 percent.”

“We are tightening the stance of policy in order to slow growth in aggregate demand. Slowing demand growth should allow supply to catch up with demand and restore the balance that will yield stable prices over time. Restoring that balance is likely to require a sustained period of below-trend growth.”

“For the near term, a moderation of labor demand growth will be required to restore balance to the labor market.”

“Growth in economic activity has slowed to well below its longer-run trend, and this needs to be sustained.”

JAN 11: Powell spoke again and stated, “Price stability is the bedrock of a healthy economy and provides the public with immeasurable benefits over time,” he said. “But restoring price stability when inflation is high can require measures that are not popular in the short term as we raise interest rates to slow the economy.”

Sounds to me that Powell still wants lower stock prices.

THE LABOR MARKET

JAN 6: Nonfarm payrolls rose 223,000 in December, as strong jobs market topped expectations. A strong jobs report is supportive of the Fed’s continued hawkish tone and is likely not desirable for the US indexes at this time.

CONSUMER PRICE INDEX

JAN 12: The Consumer Price Index for All Urban Consumers (CPI-U) declined 0.1 percent in December on a seasonally adjusted basis, after increasing 0.1 percent in November. Over the last 12 months, the all items index increased 6.5 percent before seasonal adjustment. These numbers were closely aligned with market expectations — sort of a nothing burger for the time being.

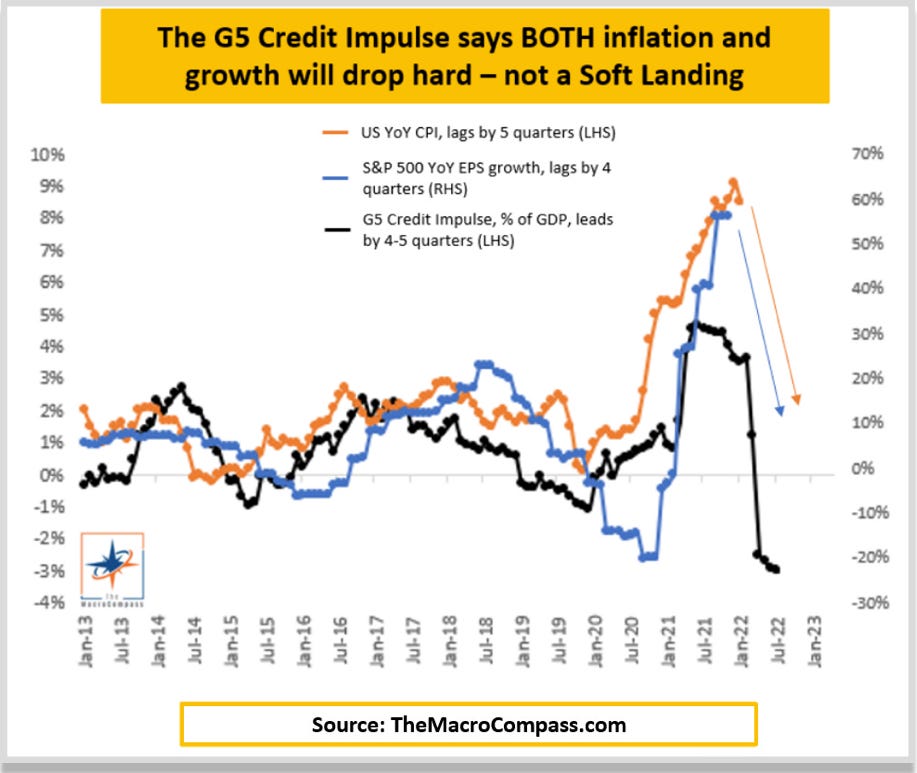

NO SOFT LANDING

With the FOMC continuing its mission of raising interest rates to slow the economy, the Fed's goal is to end that mission with a "soft landing" — that is, an economy that has slowed enough to tame inflation, but strong enough to avoid a recession.

According to

post of Jan 4, both inflation and growth are set to drop hard, suggesing a recession rather than a soft landing. This is also consistent with Powell's Jan 11 comments noted above.

HISTORICAL MARKET TRENDS

As we learned from David Rosenberg on the Macro Voices podcast #352, there are patterns that constantly reemerge in a recessionary bear market when we are close to the bottom of the cycle. Here are two:

In a recessionary bear market, the market finds its bottom as the recession itself becomes a well known, much talked about fact — this is the time when the market will start pricing in a recovery. Clearly a recession has either only just begun or has not yet even begun, so in the context of this example markets can be nowhere near a bottom if a recession is indeed on the way.

Bear market bottoms tend to occur when the Fed is ~70% into an easing cycle when interest rates have been sufficiently reduced to re-steepen the treasury yield curve; there has never been a period in history when a bear market bottomed while the Fed was still raising rates. Currently the yield curve is quite inverted along much of the duration range and the Fed is still raising rates. Again, in this context markets can be nowhere near a bottom.

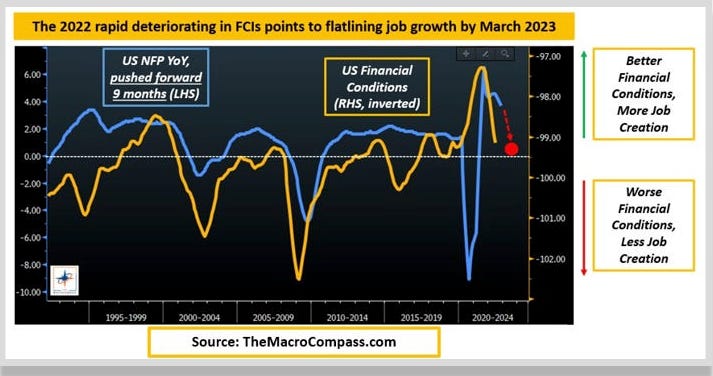

Additionally, as discussed by Financial Sense in December, market pivots are generally associated with cyclical economic or monetary pivots — this is in concert with Rosenberg’s views above. In the chart below we can see that neither the ISM Manufacturing nor the monetary indicator seems to have found a bottom, also signaling we have not yet seen the lows for the current bear market.

ADDITIONAL CHARTS

IMPACTS FOR INVESTORS

Putting it all together, from both a fundamental and technical perspective, I see the following:

US stock indexes appear to be headed lower over the course of 2023 and maybe into 2024; this is in accordance with the charts, the labor market, and the Fed themselves basically telling us this is what they want.

At some point in the year, on the back of what will eventually be a slightly more dovish Fed (maybe not lower rates, but a less-hawkish tone at least) and a potential washout of bullish sentiment, both stocks and commodities may begin a very strong multi-month cyclical bull market rally.

We have seen the first year of what is likely to be a multi-year secular bear market, likely to be characterized by wild swings in both directions, creating a lot of opportunity for the active investor.

The best portfolio for this sort of environment is likely comprised of high quality dividend-paying value stocks, select emerging market ETFs, US equity index shorts, and a substantial amount of cash or short duration cash equivalents.

As mentioned earlier, I have been taking profits to reduce my net-long exposure during the rally of the past couple weeks:

Upon seeing solid gains, I reduced my positions in the following from over-weight to equal-weight: VALE, FIVE, FCX, CTSH, INTC, DCP, TECK, TRGP, CSCO, GLW, CRI, HAS, MDT, NEM

I also began the year by adding to some of my positions:

Positions added to thus far in 2023: SDS (Short SPY), MPLX, TLT, PFE, ETR, TTEK, BMY, EPD, GSK, MSFT, EIDO, CVS, EIDO

The specific timing of all buys and sells is important; the above is provided for context only. Please do not assume that making those trades today is necessarily sensible for your portfolio. See overall allocation below for more context.

And with that, let’s dig into my Portfolio!

The below portion of this newsletter is still being offered free of charge to all my readers. Please see my About page for subscription tiers coming in March.

MY PORTFOLIO

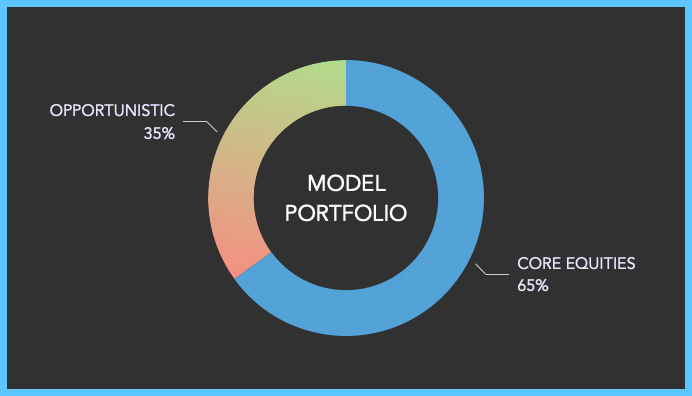

PORTFOLIO OBJECTIVE

My portfolio is designed for a specific portion of my wealth and is constructed with a total return profile, seeking capital appreciation through both dividend income and growth. My portfolio has a very strong bias toward risk management and capital preservation with the goal of providing superior risk-adjusted returns.

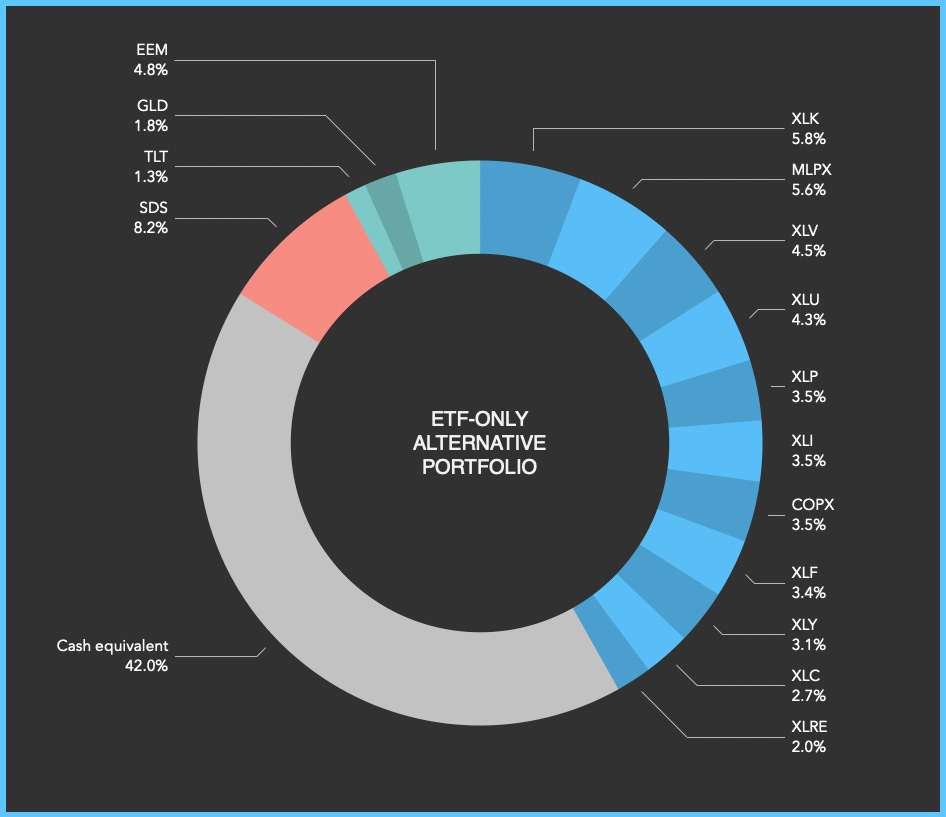

ASSET ALLOCATION

To better understand my model portfolio and investing approach, I encourage you to refer back to both my Introduction and Opportunistic Tranche articles.

CURRENT HOLDINGS

I detail my specific stock and ETF holdings in my 1st-of-the-month ‘Big Portfolio Refresh.” I will publish my next Refresh on Feb 1.

PERFORMANCE

IN CLOSING

Let’s keep the conversation going! Please comment or join my Chat, and visit my About page to learn how to contact me directly.

Thanks for the mid-month update! 2023 has gotten off to a crazy start already. Agree that it's looking more and more like a year for active portfolio management to try and stay ahead.

Trying not to get caught up in cyclical rallies as easy to forget that we're very much still in the middle of a big correction being imposed by central banks.